Will The Hawks, The Doves, Or The Cuckoos Win

By Michael Every of Rabobank

The hawks and doves are split. Tehran rejected US calls for its unconditional surrender while insulting President Trump, who stated “Nobody knows what I’m going to do,” but wants, “total and complete victory” rather than a ceasefire. The Wall Street Journal claims he’s approved attack plans but is holding the final order to see if Tehran surrenders; the New York Times suggests that might still happen, and the UK, France, and Germany are meeting Iran’s foreign minister tomorrow. Axios notes: “Trump wants to make sure such an attack is really needed, wouldn’t drag the US into a prolonged war in the Middle East – and most of all, would actually achieve the objective of destroying Iran’s nuclear program.” Others suggest he has gotten cold feet, as Israel implied it could take out the Fordow nuclear facility alone with special forces if needs be.

Yet the US is withdrawing some embassy staff from Israel and joins Russia, China, and India in telling its citizens to leave. It’s also moving regional military assets that could be hit by retaliation, as Hezbollah warned it would attack Israel and other targets if the US hits Iran. The UK –whose PM was convinced Trump wouldn’t attack days ago– is now sure he will, and The Times says he may join in, rural broadband locked and loaded, even though the attorney general who said the UK had to give the Chagos Islands to Mauritius says it could be illegal to do so.

Russian President Putin offered to mediate over Iran, but Trump told him to focus on Ukraine. There, Putin says he’s ready for substantive peace talks –after another massive drone attack– and has no plans to attack the EU or NATO, so there’s no need for anyone to spend 5% of GDP on defence. I suspect there will be few buyers – and I don’t mean for military goods.

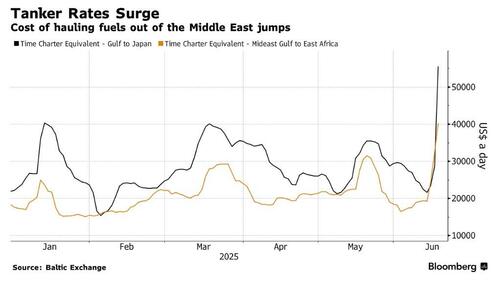

While oil is in a holding pattern, the benchmark rate for tankers moving it from the Middle East to China has risen 40% since June 13 on a higher risk premium, with further increases expected, lifting rates in other regions in tandem. Likewise, around 40% of global urea exports are at risk as Iran has shut all seven of its ammonia-urea facilities and Egypt urea production remains halted due to halted gas supply from Israel. Prices are already climbing there too.

The Fed left rates on hold at 4.50% as expected and we also have a hawk-dove clash – as Trump pondered pre-meeting if he could replace “too late” Powell as Fed Chair himself. The FOMC statement indicated uncertainty about the economic outlook has diminished(!) but remains elevated. Their projections are finally recognizing the stagflationary effects of tariffs: GDP growth was revised downward; unemployment and inflation upward. The median rate projections still showed two rate cuts in 2025, but only one cut in 2026 (down from two), but the dot plot revealed a more complicated story with two camps emerging. During the press conference Powell repeated the Committee is waiting for more clarity about trade policy and the impact of tariffs. When asked how the FOMC can state that uncertainty has diminished when there’s a war between Israel and Iran going on, Powell answered, “because of the surveys.” If that doesn’t show you the disconnect between central banks and reality, nothing will. (See here for more from Philip Marey.)

A bomb was also dropped in today’s FT op-ed by the former governor of the Indian central bank, who repeats my call of “DM = EM”. He argues without political consensus — which requires all voters to see economic gains — western institutions won’t work, so macroeconomic stability can’t be expected. Play EM games, win EM prizes. And, no, that isn’t positive for markets.

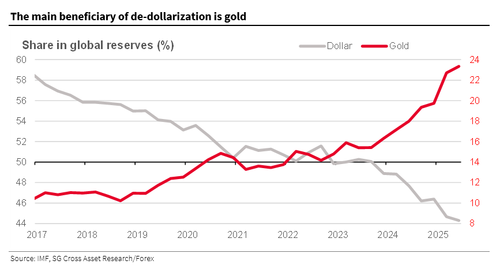

That’s as the PBOC followed the ECB in talking up their currency’s “global” role in a post-dollar world. It appears China is going to try to internationalise CNY again – without making any of the structural changes that hindered its last attempt (it just dropped to 2.9% from 3.5% in the SWIFT share, including HKD-CNY transactions); after the recent episode of Common Prosperity that shook investor confidence; and while running a trade policy described by some as “we export but don’t import”. Yet the market still appears willing to buy any narrative if it means ‘sell the dollar’.

Moreover, Bloomberg says ‘Hong Kong Dollar’s Volatility Fuels Talk on How FX Peg May Shift’, noting chatter of a shift to a basket of currencies, CNY, widening the trading range, a free float, or gold. Not so long ago, this would have created a market maelstrom. Now, not even a ‘meh’.

Yet gold is doing better than EUR or CNY or HKD with many central banks right now. Crucially, however, whereas in the past people held fiat currency as an easier way to hold underlying gold, today central banks are still holding gold as an easier way to hold underlying dollars. What else are they going to sell it for? Conch shells? Until that changes nothing really changes – and the risk is of a massive dollar short squeeze at some point; or true market chaos if the ‘post-dollar world’ ever appears rather than the polite nonsense we are seeing today.

Source: the death of fiat in one chart

Source: the death of fiat in one chartMeanwhile, the world is waiting to see if the US topples the Iranian regime and physically remakes the Middle East (again), locking its oil into the dollar system: and somehow that means the dollar is ‘over’? The disconnect in Powell’s press conference comments on Iran-Israel is replicated in the parts of the market that doesn’t see where true power sits: ‘on you, if needed’.

For example, dealmakers are unhappy that (only?) the US will use the economic statecraft Golden Share it insisted on in the Nippon Steel merger as a benchmark ahead.

The ‘EU eyes higher fees on US, British tourists to repay post-Covid debts’ (Politico), which I am *sure* won’t see a decline in visitor numbers, honest. The same article breezily notes that the EU might tax lots of other things more instead – such as small parcels coming from China. Wasn’t that the kind of thing that saw everyone selling the dollar?

China’s COSCO is in talks to join the $19bn CK Hutchison port sale: so, rather than a Hong Kong firm controlling a swathe of global ports, including at both ends of the Panama Canal, they might go to a consortium that includes a European ocean carrier (MSC) and a state-owned Chinese one? You can’t see the (geo)political issues in that “because markets” proposal?

And as New Zealand pauses funding for the Cook Islands over its recent China deal, the Australian carries an op-ed from former PM Keating arguing: “The US is running about trying to sweep gullible allies into its declining and failing pitch. Yet, it believes there is always a mug who will buy its venal view of affairs. And in Australia, the US is not disappointed. The Australian Labor Party, at its grassroots, will not support Australia being dragged into a war with and by the US over Taiwan, “ and talks of “a careless betrayal of the country’s policy agency and independence in its ability to make decisions in its own national interest and not in the interest or interests of another country.” That just screams to sell USD and buy AUD, right?

Yet it’s The Economist which outdoes itself today in being neither hawk nor dove, but cuckoo. It argues “Investors ignore world-changing news. Rightly” in “The Nothing Ever Happens Market”. Until it does, on multiple fronts, from Iran to the Fed, and from trade flows to financial architecture, and then investors can’t. To be frank, this 30-something, smug, DM financial market/media argument sounds like the kind of stereotypical self-satisfied, privileged echo-chamber babble that EM banana republic elites live in right up until the peasants start revolting – which they always think they are. I’m with the FT op-ed on what this means for central bankers.

The Nothing Ever Happens Market: Economist

The Nothing Ever Happens Market: EconomistThat’s as Brazil hiked rates 25bps to 15% against market expectations, and today has the BOE, which will attempt to Keep Calm and Rates On Hold: but will it again speak out against the populist Reform Party’s fiscal plans four years ahead of an election?

Tyler Durden

Thu, 06/19/2025 – 18:55

![Nowi funkcjonariusze zasilą szeregi policji [ZDJĘCIA]](https://cowkrakowie.pl/wp-content/uploads/2025/06/policja11.jpg)