Watch Live: „Very Dumb” Fed Chair Testifies To Congress

Watch Fed Chair Powell’s testimony to Congress here (due to start at 1000ET):

* * *

In his prepared remarks ahead of this morning’s Humphrey-Hawkins testimony to Congress, Fed Chair Powell reiterated his comments from last week’s FOMC that the central bank is in no rush to lower interest rates as officials wait for more clarity on the economic impact of President Donald Trump’s tariffs.

“The effects of tariffs will depend, among other things, on their ultimate level,” Powell said Tuesday in remarks prepared for delivery to Congress.

“For the time being, we are well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.”

His comments – with no a bit of dovishness – comes after three of his colleagues (Waller, Bowden, and Goolsbee) all hinted at rate cuts as soon as July in recent days.

Powell said the tariffs’ impact on inflation could be short-lived or possibly be more persistent.

“Expectations of that level, and thus of the related economic effects, reached a peak in April and have since declined,” Powell said in a statement that largely echoed remarks he delivered last week.

“Even so, increases in tariffs this year are likely to push up prices and weigh on economic activity.”

Avoiding the latter outcome “will depend on the size of the tariff effects, on how long it takes for them to pass through fully into prices and, ultimately, on keeping longer-term inflation expectations well anchored,” he said.

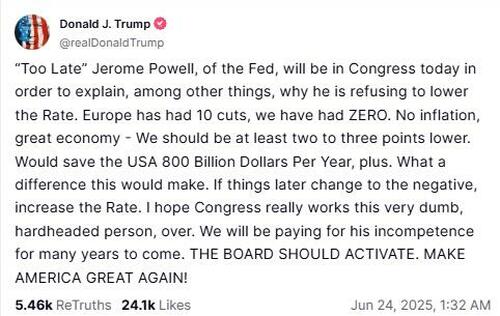

President Trump chimed in (early):

“‘Too Late’ Jerome Powell, of the Fed, will be in Congress today in order to explain, among other things, why he is refusing to lower the Rate,” Trump said on social media early Tuesday.

“I hope Congress really works this very dumb, hardheaded person, over. We will be paying for his incompetence for many years to come.”

Economic data so far has shown limited impact from tariffs.

Does make you wonder about „Fed Independence”…

Powell: Inflation Has Eased Significantly but Remains Somewhat Elevated

is it somewhat less elevated than it was in Sept 2024 when you cut 50 bps to ram stocks higher into the election?

— zerohedge (@zerohedge) June 24, 2025

* * *

Read Powell’s full prepared remarks below:

Chairman Hill, Ranking Member Waters, and other members of the Committee, I appreciate the opportunity to present the Federal Reserve’s semiannual Monetary Policy Report.

The Federal Reserve remains squarely focused on achieving our dual-mandate goals of maximum employment and stable prices for the benefit of the American people. Despite elevated uncertainty, the economy is in a solid position. The unemployment rate remains low, and the labor market is at or near maximum employment. Inflation has come down a great deal but has been running somewhat above our 2 percent longer-run objective. We are attentive to the risks to both sides of our dual mandate.

I will review the current economic situation before turning to monetary policy.

Current Economic Situation and Outlook

Incoming data suggest that the economy remains solid. Following growth of 2.5 percent last year, gross domestic product (GDP) was reported to have edged down in the first quarter, reflecting swings in net exports that were driven by businesses bringing in imports ahead of potential tariffs. This unusual swing has complicated GDP measurement. Private domestic final purchases (PDFP)—which excludes net exports, inventory investment, and government spending—grew at a solid 2.5 percent rate. Within PDFP, growth of consumer spending moderated, while investment in equipment and intangibles rebounded from weakness in the fourth quarter. Surveys of households and businesses, however, report a decline in sentiment over recent months and elevated uncertainty about the economic outlook, largely reflecting trade policy concerns. It remains to be seen how these developments might affect future spending and investment.

In the labor market, conditions have remained solid. Payroll job gains averaged a moderate 124,000 per month in the first five months of the year. The unemployment rate, at 4.2 percent in May, remains low and has stayed in a narrow range for the past year. Wage growth has continued to moderate while still outpacing inflation. Overall, a wide set of indicators suggests that conditions in the labor market are broadly in balance and consistent with maximum employment. The labor market is not a source of significant inflationary pressures. The strong labor market conditions in recent years have helped narrow long-standing disparities in employment and earnings across demographic groups.

Inflation has eased significantly from its highs in mid-2022 but remains somewhat elevated relative to our 2 percent longer-run goal. Estimates based on the consumer price index and other data indicate that total personal consumption expenditures (PCE) prices rose 2.3 percent over the 12 months ending in May and that, excluding the volatile food and energy categories, core PCE prices rose 2.6 percent. Near-term measures of inflation expectations have moved up over recent months, as reflected in both market- and survey-based measures. Respondents to surveys of consumers, businesses, and professional forecasters point to tariffs as the driving factor. Beyond the next year or so, however, most measures of longer-term expectations remain consistent with our 2 percent inflation goal.

Monetary Policy

Our monetary policy actions are guided by our dual mandate to promote maximum employment and stable prices for the American people. With the labor market at or near maximum employment and inflation remaining somewhat elevated, the Federal Open Market Committee (FOMC) has maintained the target range for the federal funds rate at 4-1/4 to 4-1/2 percent since the beginning of the year. We have also continued to reduce our holdings of Treasury and agency mortgage-backed securities and, beginning in April, further slowed the pace of this decline to facilitate a smooth transition to ample reserve balances. We will continue to determine the appropriate stance of monetary policy based on the incoming data, the evolving outlook, and the balance of risks.

Policy changes continue to evolve, and their effects on the economy remain uncertain. The effects of tariffs will depend, among other things, on their ultimate level. Expectations of that level, and thus of the related economic effects, reached a peak in April and have since declined. Even so, increases in tariffs this year are likely to push up prices and weigh on economic activity.

The effects on inflation could be short lived—reflecting a one-time shift in the price level. It is also possible that the inflationary effects could instead be more persistent. Avoiding that outcome will depend on the size of the tariff effects, on how long it takes for them to pass through fully into prices, and, ultimately, on keeping longer-term inflation expectations well anchored.

The FOMC’s obligation is to keep longer-term inflation expectations well anchored and to prevent a one-time increase in the price level from becoming an ongoing inflation problem. As we act to meet that obligation, we will balance our maximum-employment and price-stability mandates, keeping in mind that, without price stability, we cannot achieve the long periods of strong labor market conditions that benefit all Americans.

For the time being, we are well positioned to wait to learn more about the likely course of the economy before considering any adjustments to our policy stance.

To conclude, we understand that our actions affect communities, families, and businesses across the country. Everything we do is in service to our public mission. We at the Fed will do everything we can to achieve our maximum-employment and price-stability goals.

Tyler Durden

Tue, 06/24/2025 – 10:00

![Nielegalna bimbrownia. Policjanci zabezpieczyli prawie 2000 litrów alkoholu [ZDJĘCIA]](https://static2.supertydzien.pl/data/articles/xga-4x3-pow-zamojski-nielegalna-bimbrownia-policjanci-zabezpieczyli-prawie-2000-litrow-alkoholu-zdjecia-1750797675.jpg)