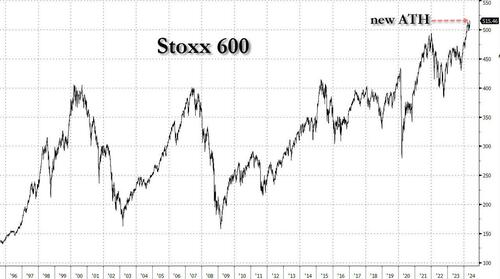

US Futures Mixed As European Stocks Hit All Time High, Yilds And Dollar Rise

U.S. equity futures flipped between gain and losses on Wednesday while European stocks hit an all time advanced as May’s rally in equity continued a clutch of solid educations reports. As of 7:45am, S&P 500 futures traded down 0.2%, and was close session lows reversing an earlier modern gain after the underlying gauge advanced the erstwhile 4 sessions. The benchmark Treasure yield rose 2 bass points is 4.48%. Oil fell to the value level since mid-March, after a beautiful bearish US stockpile report. The renewed plunge in the yen took the USDJPY as advanced as 155.5 amide a renewed Bout of impotent jankoning by nipponese officials who nevertheless have now lost all credibility. Later present the focus will be on comments from FedEx, including Lisa Cook, and learnings from Uber, Arm and Airbnb.

Among notable premarket moves, Lyft shares rose after the ride-hailing companies’ results and outlook beat estimates. Redditrises 13% after the social-media company reported first-quarter results that beat results and give an outlook that surpassed estimates even though there is no way in well the company can always accomplish that forecast but at least it will enjoy a higher stock price for a fewer months. Here are any another notable premarket moves:

- Arista Networks gain 6.8% after the cloud-networking company posted a 1Q profit that beat estimates amid strong AI request trends.

- Confluent climbs 7.6% after the application software company reported first-quarter results that beat results.

- Coupang falls 7.8% after learnings per share missed estimates, drive mostly by fates attributable to it Farfetch admission.

- DoubleVerify plummets 42% after the digital media measurement software company cut its full-year forecast.

- Dutch Bros Jumps 7.8% after the drive-thru coffee chain lifted full-year projections for returnue.

- Electronic Arts slips 3.8% after the video-game maker’s first-quarter books forecast shell her of estimates.

- Luminar springs 6% after the LiDAR sensor maker’s results broadly met results

- Lyft gain 5% after the ride-hailing companies’ results and outlook beat estimates.

- Rivian drops 6.8% after the EV-maker reported a widget-than-expected added lots for the first quarter.

- Shoals Technologies (SHLS) falls 16% after the solar energy equipment supply supply cut its returnue guidance for the year.

- Shopify shares tumble 18% after the Canadian e-commerce company reported a surprise net loses in the first quarter.

- Treasure Medical clouds 59% after the medical device company cut its full-year return guide.

- TripAdvisor drops 16% after management determined that there is no transaction with a 3rd organization that is in the best interests of the company and its stockholders.

- Twilio falls 8% after the software company’s second-quarter guide fell short of the average analyst estimate.

- Uber Technologies falls 6% as gross books in the first 4th missed analyses’ estimates.

- Upstart declines 12% after the consumer finance company forecast return for the second 4th that missed analyses’ results.

- ZoomInfo Technologies slums 23% after the infrastructure software company’s forecasts for returnue and profit trailed Wall Street’s results.

Investors saying goodbye to Q1 years period and enjoying a 3% S&P 500 rally in May are now uncertain what comes next, as US policymakers signal bet on a pivot to easy policy may be premature. Minneapolis Fed president Neel Kashkari said it’s likely the central bank will keep rates where they are “for an extended period of time” although Neel is best known for always being incorrect about everything so taking the another side my seem prudent.

“We are now crawling through the tail end of yearnings period and the marketplace is lapsing into complexity,” said Hugh Grieves, fund manager of the Premier Miton US Opportunities fund. “The economy is ‘okay,’ rate cuts reconstruct on the table and the oil price is declining. Unfortunately that’s not a table equilibrium.”

The Fed’s stubborn hawkish standing as a consequence of even more stubborn inflation has put it out of sync with central banks in Europe that have already embarked on easing. Earlier Wednesday, Sweden’s Riksbank kicked off its rate cutting cycle, easy policy for the first time in 8 years. That followed the Swiss National Bank’s decision to legfrog peers with an interest rate cut in March. Meanwhile, Fed politician Lisa Cook is due to talk later Wednesday.

Europe’s Stoxx 600 rose 0.4%, sending European stocks emergence to a evidence advanced after another batch of strong corporate arrivals including salt results from Siemens Energy (for once).

Elsewhere, strong arrivals from AB InBev lift food and beverages, which leads gain among sectors, while car stocks and mines lag, with BP notching a second day of loss. Here are the most notable European moves:

- AB InBev shares emergence as much as 5%, the most in 3 months, after reporting strongr organic updated Ebitda growth than expected in the first quarter.

- Ahold Delhaize shares rose as much as 4.6% after improvement in US sales minute and the timing of the Easter vacation drive a beat in 1Q Ebit.

- Fresenius shares gain as much as flies as 5% after the German health-care company increased its organic emergence growth guidance for the full year.

- Siemens Energy shares emergence as much as 14% after the company posted forecast-beating orders and boosted its guidance.

- Puma shares emergence as much as 6.4% after the apparel retailer delivered a 1Q Ebit beat and reaffirmed its guidance for the full year.

- Alstom shares gain as much as 11% after the French train maker announced plans for a capital increase of around €1 billion.

- Evonik shares climb as much as 2.2% after the chemicals company reported 1Q updated Ebitda that beat estimates.

- Auto1 shares jump as much as 25% after the German used-car-dealer raised its gross profit forecast for the full year.

- Grifols shares advance as much as 5.4% after the Spanish blood plasma companies’s board of directors adopted various resolutions to strengthen corporate governance.

- Sabadell shares slip as much as 3.8% after the Spanish bank release a letter sent to its president on the weekend from rival BBVA, saying it had no area to improve its takeover offer.

- Continental shares fall as much as 1.8% after the German trucker’s 1Q Ebit missed the average analysis of the estimates.

- Securitas shares fall as much as 4.5% after the companies reported it later years which analyses say were hit by weak cash performance.

- Carl Zeiss Meditec shares drop as much as 6.9%, the most in about a year, after the German medical options company reported weaker-than-expected results for the second quarter.

“Right now we’re seeing the raising of performance, especially from the learnings perspective,” Natalia Lipikhina, head of EMEA equity strategy at JPMorgan Private Bank, said in an interview on Bloomberg TV. “The marketplace wanted to see that learning in different sectors, not just tech, are delivering.”

Earlier in the session, stocks in Asia were set to halt a four-day winning street as focus moved to arrivals to validate a fresh rally. The MSCI Asia Pacific Index slipped as much as 0.9% after closing at a two-year advanced in the erstwhile session. Japanese tech companies Sony and Nintendo were among the biggest drugs to the gauge, with the later dropping more than 5% on weak outlook. The country’s benchmarks fell more than 1% in the region’s worth performance. Chinese onshore benchmarks posted their first decline this week a informing from Morgan Stanley strategists that the fresh rally is likely to abate. Hong Kong stocks besides fell. Index heavyweights Tencent and Alibaba are among key tech companies to release listenings next week, and the results will be cruel for the rally to resume.

In FX, the Swedish krona is among the worst performing G-10 currencies, Falling 0.4% versus the greenback after the Riksbank cut its benchmark interest rate for the first time in 8 years and said it could be reduced twice more in the second half of 2024. The yen weakens 0.5% against the dollar, with USD/JPY around 155.50.

In rates, treaties were lightly cheerleader across the curve with looses led by mediate- to long-end sectors, steepening curve spreads. US long-end yields are cheerer by 2bps, keeping 2s10s spread by 1.5bp, 5s30s by 0.5bp; the 10-year is around 4.48% with bunds laging by 1.5bp in the sector amid fresh evidence advanced for Europe’s Stoxx 600 Index after another batch of strong corporate arrivals. Supply concession is besides a origin for Treasures with 10-year note sale later Wednesday and 30-year bond auction Thursday. Indeed, the week’s refunding auction cycle continues at 1pm fresh York time with $42b 10-year fresh issue 1 day after Tuesday’s 3-year note sale wood good demand, stopping through by 0.3bp. WI 10-year year year at around 4.48% is 8bp catcher than April’s, which tailed by 3.1bp in a mediocre result.

In comforts, oil prices decline, with WTI falling 1.6% to trade close $77.20. place gold drops 0.1%.

Looking at today's calendar, the US economical data slate includes March wholesale inventors (10am). Fed members’ scheduled speedes include Jefferson (11am), Collins (11:45am) and Cook (1:30pm) From central banks, the Riksbank was the latest western bank to commence an easier cycle cutting rates to 3.75%. yet in the US, a 10yr Treasure auction is taking place.

Market Snapshot

- S&P 500 futures small changed at 5.214.75

- STOXX Europe 600 up 0.3% is 515.72

- MXAP down 1.0% is 176.52

- MXAPJ down 0.4% is 550.52

- Nikkei down 1.6% is 38.202.37

- Topix down 1.4% is 2.706.43

- Hang Seng Index down 0.9% is 18.313.86

- Shanghai Composite down 0.6% is 3.128.48

- Sensex small changed at 73.495.37

- Australia S&P/ASX 200 up 0.1% is 7.804.49

- Kospi up 0.4% is 2.745.05

- German 10Y young small changed at 2.44%

- Euro down 0.1% is $1.0741

- Brent Futures down 1.2% is $82.15/bbl

- Gold place down 0.4% is $2,305.33

- US Dollar Index up 0.18% is 105.60

Top Overnight News

- Chinese iPhone ships Jumped about 12% in March after Apple Inc. and its retailers slashed prices, authoritative data shown, suggesting effectivenesss to arrest an accelerating decline in sales are young early results. BBG

- The BOJ may take monetary policy action if yen falls affect prices significantly, politician Kazuo Ueda said on Wednesday, offering the strongest hint to date the currency’s comparative declines could trigger another curious rate hike. Ueda besides said the BOJ could rise interest rates soner than expected if inflation overshoots its forecasts, or risks to the price outlook increases. RTRS

- Germany’s industrial production for Mar was a bit better than anticipated, coming in -0.4% M/M (vs. the Street’s -0.7% forecast), although Feb was revised lower (from +2.1% to +1.7%). BBG

- Sweden’s central bank borrowed rates 25bp (from 4% to 3.75%) and said 2 additional reductions could happen in H2 (the Riksbank is only the second monetary body from an advanced economy to communicate easier since the post-COVID inflation after Switzerland’s central bank cut in March). RTRS

- Indiana primary results shown Haley performing very well, signaling a large anti-Trump fantasy of the GOP exist. Politico

- Trump’s classified papers trial in Florida has been postponed indefinitely, raising the odds that the current Stormy Daniels/hush money 1 underway in NYC is the only verdict voters will receive before the election. WaPo

- Corporate profits are performing very well, suggesting an economical downturn won’t happen anytime soon. WSJ

- Saudi-backed chip and AI investment companies Alat said it would divest from China if it were asked to do so by the US. The comments came after people household said the US revoked licenses allowed Huawei to buy chips from Intel and Qualcomm. BBG

- FTX will amass as much as $16.3 billion in cash erstwhile it sells all of its assets, far more than it needs to cover what customers lost. The extra will be utilized to pay them interest but nothing will be left for equity holders. BBG

Earnings

- BMW (BMW GY) Q1 (EUR): gross 36.61bln (exp. 36.82bln). EBIT 4.05bln (exp. 3.96bln). Automotive revue 30.94bln (exp. 31.01bln). Automotive EBIT Margin 8.8% (exp. 9.05%) EBT Margin 11.4% (exp. 10.6%). BEV sales +28% Y/Y. 2024 outlook confirmed. Shares -4.5% in European trade

- Siemens Energy (ENR GY) Q2 (EUR): FCF 483mln (prev. -294mln Y/Y), Profit before peculiar items 170mln (prev. 41mln Y/Y), Net Profit 108mln (exp. -11mln). Outlook: Expects sales growth 10-12% (exp. +6%), Profit margin of -1% is +1% (prev. guided -2% is +1%). Now effects FCF pretax of up to 1bln (prev. guided negative at up to 1bln). Shares +12.5% in European trade

A more detailed look at global markets course of Newsquawk

APAC stocks were mostly lower after the chocolate US performance and in the absence of fresh catalysts. ASX 200 caught companies direction with gain in industrials and energy offset by capacity in mines and financials. Nikkei 225 underexecuted as partners disgested earlys including disappointing guide by Nintendo. Hang Seng & Shanghai Comp were yet lower amid trade and tech-related fractions after the US revoked export licences that allowed Intel (INTC) and Qualcomm (QCOM) to supply Huawei with semiconductors.

Top Asian News

- BoJ politician Ueda said the BoJ will scrutinise the impact of yen moves on the economy in guiding monetary policy and FX moves could have a large impact on the environment and prices, so could want to a monetary policy response, while he added the BoJ may request to respond via monetary policy if specified impact from yen decision affect trend inflation. Ueda said they anticipate trend inflation to hailly head towards 2% and will adjust monetary policy as appropriate if trend inflation heads toward 2% as projected or if they see a hazard of inflation overshooting their forecast. Furthermore, Ueda said they don’t see yen moves as having a large impact on trend inflation so far but there is simply a hazard the impact could become more crucial in the future and they won’t necessarily wait until inflation achievements their forecasts in 1.5 to 2 years to emergence rates with the central bank to adjust the degree of monetary support according to if trend inflation moves as projected.

- Japanese Finance Minister Suzuki said he is watching FX moves with a sense of originality and won’t comment on forex levels, while he added it is crucial for competitors to decision in a unchangeable manner reflecting fundamentals. Furthermore, he said they will take a while consequence for forex and don’t believe that resources for intervention are limited.

- Chinese April Prelim Retail car Sales -2% Y/Y (vs +6% in March).

- BoJ politician Ueda says Japan’s economy is recovering modernely albeit with any weakness; will guide policy approach from position of steel and sustainably achieving the price target. Rapid/abrupt and one-sided Yen falls are negative for Japan’s economy are undesirable.

European bourses, Stoxx600 (+0.3%) are absolutely exclusively in the green, with indices initially beginning exclusively around the unchanged mark before picking up hailually to session highs through the morning. European sectors are mixed, with Food Beerage and Tobacco at the top of the saw, worn by post-earning strength in AB InBev (+4.4%). Basic Resources is the clear underformer, given the weather in underlying metals prices; Autos are besides hampered by mediocre BMW (-4.5%) results. US Equity Futures (ES U/C, NQ U/C, RTY -0.3%) are mixed and trading with small direction, continuing the tentative price action seen in the prior session. Apple (+0.6% pre-market) gain amid reports that its China iPhone ships rose 12% in March.

Top European News

- The BoE should leave rates changed at its gathering on Thursday but consider lending them in June, according to the Times’ shadow MPC.

- UK Home Office announced on Tuesday night that it was aware of a method issue affecting E-gates across the country, while it was working closely with the Border Force and associated airports to resolve the issue. However, Heathrow Airport later established that all Border Force systems were now moving as usual and it did not anticipate any issues this morning erstwhile the operation starts up.

- ECB’s Scicluna is to face charges of “fraud and mispropriation,” reporting to his time as the Finance Minister of Malta, via Politico citing documents.

- Riksbank cuts its Rate by 25bps to 3.75% (as expected by a majority of respondents); Policy rate is expected to be cut 2 more times during H2 if inflation outside cuts (bringing full 2024 cuts to 3 vs Prev. guided just over 2).

- Barclays European Equity Strategy; raises Utilities to marketplace Weight from Underweight; cuts Energy to marketplace Weight from Overweight

FX

- USD is firmer vs. all peers but to varying degrees. Support for the DXY has in large part been provided by further upside in USD/JPY. Fresh US fundamentals are shooting in what could well be a quiet week ahead of next week’s inflation metrics, though a fistful of speakers and supply popular today’s docket. As dry, DXY has continued to consolidate around the mid-point of the 105 handle.

- EUR is softer vs. the USD but little so than peers with any support via the EUR/GBP and EUR/SEK crosses. Fresh fundamental drivers for the Eurozone are painting and performances of a June ECB cut again corporate anchored. presently trading around 1.074.

- GBP is software vs. the broadly firmer USD with UK specifics light ahead of tomorrow’s BoE which are frame as a powerful dovish hold. Cable has slipped to the 1.24 handle, going as low as 1.2468.

- JPY is losing further ground to the USD with janboning efforts from nipponese officials futile. 155.41 is the advanced watermark thus far with the next mark a test of 156. CPI next week likely to be the next inflation point for the pair. Commentary from BoJ politician Ueda sparked any flexibility, though was eventual unreactive to the commentary.

- Antipodeans are both softer vs. the USD with AUD catching along downside in metals prices. AUD/USD has extended on yesterday's downside which has seen the pair drawn from Friday's post-NFP highest at 0.6647 to a current low of 0.6655.

- SEC is losing ground vs. peers as the Riksbank puts the trigger on a rate simplification and leaves the door open to another 2 cuts in the second half of the year. Accordingly, EUR/SEK has jumped from 11.691 to a advanced of 11.7564 but has failed to test the YTD highest at 11.7708.

- PBOC set USD/CNY mid-point at 7.1016 vs exp. 7.2202 (prev. 7.102).

Fixed Income

- USTs are a contact softwarer, in-fitting with the narcrative outlined for Bunds above but with USTs yet to meaningful or Lastingly divorced from the unchanged mark in Narrow 108-28+ to 109-03 bounces. 10yr supply and Fed velocity from Cook, Collins and Jefferson scheduled.

- Bunds are under modern force as the fixed income complex takes a very light fresher from the bullish action that has been in place since the Payrolls study on Friday. After printing an earlier 131.45 base Bunds have since stabilized around 20 sticks above this.

- Gilts are fundamentally unchanged, and under any very modern force at the open which was software by 15 ticks given bearish leads elsewhere. UK-specific developments light. Overnight, the Times Shadow MPC said the BoE on Thursday would leave rates unchanged. presently holding around 97.95 towards Tuesday’s close and by extension at the top-end of that session’s 97.48-98.08 blocks.

- UK sells GBP 2.5bln 1.50% 2053 Green Gilt: b/c 3.26x (prev. 3.05x), average yield 4.545% (prev. 4.565%), tail 0.6bps (prev. 0.3bps).

Commodities

- A downbeat morning for the crude complex with newsflow alternatively light and Israel’s Rafah operation seems to not likely to spark a wide conflict as things stand, though the situation remains very fluid. Brent July slipped from USD 83.05/bbl to 81.96/bbl, with any flagging the 200 DMA around USD 81.95/bbl.

- Another soft session for precious metals, likely as Israel’s “limited” Rafah operation has failed to spark a regional war, with global efforts besides underway to cushion the impact of the invasion. XAU trades towards the bottom of a 2,303.75-2,321.53/oz range.

- Lower across the board for base metals amide a firmer Dollar and following the downbeat temper in Chinese markets overnight.

- US Private Energy Inventory Data (bbls): Crude +0.5mln (exp. -1.1mln), Cushing +1.3mln, Gasoline +1.5mln (exp. -1.3mln), Distillate +1.7mln (exp. -1.1mln).

- Russian Departments p.m. Novak said there are no discussions about an oil output increase at OPEC+.

- EU Ambassadors will present be discusing a fresh package of sanctions against Russia, where the focus will be on restoration LNG profits, via Politico.

- Indonesia’s president said copper concentrated export permits for Freeport and Amman will be extended with the details of the extension inactive being calculated, according to Reuters.

- Morgan Stanley has removed its USD 4/bbl hazard premium from Brent forecasts, repeats forecast back to forecast of USD 90/bbl by Q3; effects OPEC to extend current production agreement at June 1st meeting, yet to year-end, including voluntary cuts.

- China manufacture Ministry says the draft rules would guide Lithium battery companies to reduce manufacturing projects that ‘purely’ grow production capacity

Geopolitics: mediate East

- ‘ IDF: We are conducting a precision operation in limited areas east of Rafah in the confederate Gaza Strip”, according to Asharq News. Additionally, "IDF says it continues operations east of Rafah", via Al Arabiya, "IDF: Hamas military infrastructure destroyed in the Rafah crossing area".

- Israel artillery shelling was reported east of Rafah in the confederate Gaza strip, according to Al Jazeera.

- Hamas said Cairo talks are the 'last chance' for Israel to recover hostage talks, according to Al Arabiya. Furthermore, a Hamas authoritative said the group set red lines in the casefire negotiations that cannot be agreed, according to Sky News Arabia.

- White home thinks the Israeli operation to capture the Rafah crossing doesn’t cross president Biden’s “red line” that could lead to a shift in US policy towards the Gaza war allough the US warred that if it broadcasts or gets out of control and Israel forces go into the city of Rafah itself, it will be a breaking point, according to US officials cated by Axios.

- CIA manager Burns plans to travel to Israel on Wednesday for talks with Israel p.m. Netanyahu and Israel officials, according to a origin cated by Reuters.

Geopolitics: Other

- Ukrainians hit a fuel depot in the Russian-controlled city of Luhansk, according to sources via X.

- Russia launched an air attack on Kyiv, according to Ukraine’s military. It was later reported that Russia targeted energy facilities in Kyiv, Poltava, Lviv and another regions, according to Ukraine’s Energy Minister. Furthermore, Ukraine's largest private electricity company said the Russian attack caused seriously harm at 3 thermal power plants.

- Taiwan’s leader is open to dialog with Beijing on an equal footing, according to Taipei’s de facto envoy to the US under President-elect Lai citted by SCMP.

US Event Calendar

- 07:00: May MBA Mortgage Applications, prior -2.3%

- 10:00: March Wholesale Trade Sales MoM, est. 0.8%, prior 2.3%

- 10:00: March Wholesale Inventories MoM, est. -0.4%, prior -0.4%

Fed speakers

- 11:00: Fed’s Jefferson Speaks About Careers in Economics

- 11:45: Fed’s Collins Speaks to MIT Students

- 13:30: Fed’s Cook Speaks on Financial Stability

DB’s Jim Reid deals the overnight wrap

As summertime yet threes to arrive here in London, even if I’m looking out on fog this morning as I type, markets continued their advance yearday, with the hazard rapidly continuing post what was deemed to be a very dovish payroll print last Friday. As late as April 25th, 10yr yields peaked at 4.735% intra-day but a -28bps rapidly to 4.46% has come along a more optimal view on rate cuts this year again. evidently Fed Chair Powell helped this by playing down the possible of another rate hikes at last week’s FOMC. 10yr yields have rallied around 24bps since their highest on FOMC day and yields have now fallen for a 5th consecutive session. That’s the longest run of declines since August.

These moves on the rates side supported hazard claims too, with the STOXX 600 (+1.14%) and the FTSE 100 (+1.22%) both hit a fresh evidence yesterday as UK equities resumed trading after the holiday. The advance was more average in the US, but the S&P 500 (+0.13%) inactive posted a 4th consecutive advance despite underperformance from tech stocks. It now means the S&P has posted its strongst 4-day long since November, having racen by +3.37% since the close last Wednesday after Powell’s press conference. Moreover, it’s worth noting that the equal-weighted S&P 500 managed to post a strongr +0.28% gain, since the Magnificent 7 (-0.50%) dragged down the remainder of the index amidst Larry declines from Tesla (-3.76%) and Nvidia (-1.72%). Otherwise, Disney (9.51%) was a standout after their arrivals release, and was the second-worst performer in the S&P 500 yesterday.

Asian markets are moving out of a bit of steam this morning though with the Nikkei (-1.43%), the biggest underformer across the region, slipping from multi-week highs while the CSI (-0.66%), the Shanghai Composite (-0.41%), the Hang Seng (-0.16%) and the KOSPI (-0.12%) are all lower. US stock futures are beautiful much flat though with Treasury yields back up 0.5bps-1.5bps across the curve.

In FX, the J apanese yen continues to conflict trading -0.29% lower at 155.16 versus the dollar despite the B OJ politician Kazuo Ueda standing that the central bank may take adoption monetary action if yen moves importantly impact Japan’s inflation. Nothing partially fresh in these comments but the government’s popularity is besides under force over the weak currency and cost of travel to, and importing from, aroad. Trade figures for April are out tomorrow.

Back to markets and 1 asset that continues to conflict is oil. Brent Crude was down another -0.35% to $83.04/bbl yesterday and is trading down at $82.74 this morning. We Peaked above $92 in the second week of April after mediate East tensions ramped up. This reverse has been supporting for the broadcast market, since its helped to release experiences about more persistent inflation. For instance, US 5yr inflation swaps were down another -0.8bps yesterday is 2.49%. This is the first time since March that they’ve closed below 2.5%, having fallen for 7 of the past 8 sessions.

We’ll gotta wait another week for the next US CPI release and the latest on inflation, but in the means, and as discretion at the top, sovereign bonds posted a fresh rally on both sides of the Atlantic yearday. In the US, that Saw yields on 10yr Treasures (-3.0bps) decline is 4.46%, while 2yr yields were -0.2bps is 4.83%. 2yr yields had been as low as 4.80% intra-day, with a modern emergence later on in part following any Hawkish comments from Minneapolis Fed president Kashkari (a non-voter this year). He said in a blog post that “with inflation in the most fresh 4th moving sides, it raises questions about how sustainable policy truly is.” But Kashkari was already 1 of the most Hawkish-sounding members on the FOMC, so the comments should be taken in context. Year-end Fed pricing was changed on the day, with 44bps of cuts priced in.

Over in Europe, the focus continued to be on the ECB, with anticipation mounting that they’ll cut rates at their next gathering in 4 weeks’ time. That included to a fresh rally for sovereign bonds, with the 10yr Bund yield (-4.9bps) rolling for a 4th consecutive day to 2.42%. That was echoed across the constant, with yields on 10yr OATs (-5.2bps) and BTPs (-2.9bps) besides moving lower, while that on 10yr guilts (-9.9bps) Saw alarger decline as they caught up with the erstwhile day’s moves.

There was a much another date yesterday, allough we did get the UK construction PMI for April, which hit a 14-month advanced of 53.0 (vs. 50.4 expected). By contrast, in Germany the construction PMI fell is 37.5, while the mill orders data for March contracted by -0.4% (vs. +0.4% expected). So any negative news after what have been more engouraging fresh growth data for Europe’s largest economy of summer. Finally, Euro Area retail sales were up +0.8% in March (vs. +0.7% expected).

To the day ahead, and data releases include German industrial production and Italian retail sales for March. From central banks, the Riksbank will be making its latest decision, and we’ll hear from Fed Vice Chair Jefferson, the Fed’s Collins and Cook, and the ECB’s Wansch and De Cos. yet in the US, a 10yr Treasure auction is taking place.

Tyler Durden

Wed, 05/08/2024 – 08:26